Is Now a Good Time to Invest in Real Estate?

-

Mortgage rates have drifted down to about 6.30% for a 30-year fixed as of October 9, 2025 (Freddie Mac PMMS), improving affordability versus late 2023–mid 2024 peaks. (Freddie Mac)

Home prices remain resilient: NAR puts the August 2025 median existing-home price at $422,600 (+2.0% YoY) with 4.6 months’ supply, while the Case-Shiller index remains near record territory. (National Association of REALTORS®)

Rental fundamentals show a higher vacancy rate (7.0% in Q2 2025) after an unprecedented surge in multifamily completions in 2024; new supply is slowing in 2025, which should gradually firm rent growth in many markets. (Census.gov)

Peer-reviewed evidence suggests housing offers competitive long-run real returns comparable to equities and can hedge inflation (especially in stable regimes), although short-term hedging is mixed. (OUP Academic)

Bottom line: If your time horizon is multi-year, and you buy quality assets at disciplined yields (or with a credible value-add plan), 2025 is shaping up as a reasonable entry point—especially in multifamily submarkets where supply is peaking and financing is available. If your strategy requires short-term flips or heavy leverage, you’ll need to be pickier on basis and underwriting.

Where the market stands right now

Mortgage rates: easing from the highs, still elevated historically

The 30-year fixed rate averaged 6.30% in the week ending October 9, 2025, down from 6.34% a week earlier and well off 2023’s peaks. (Freddie Mac)

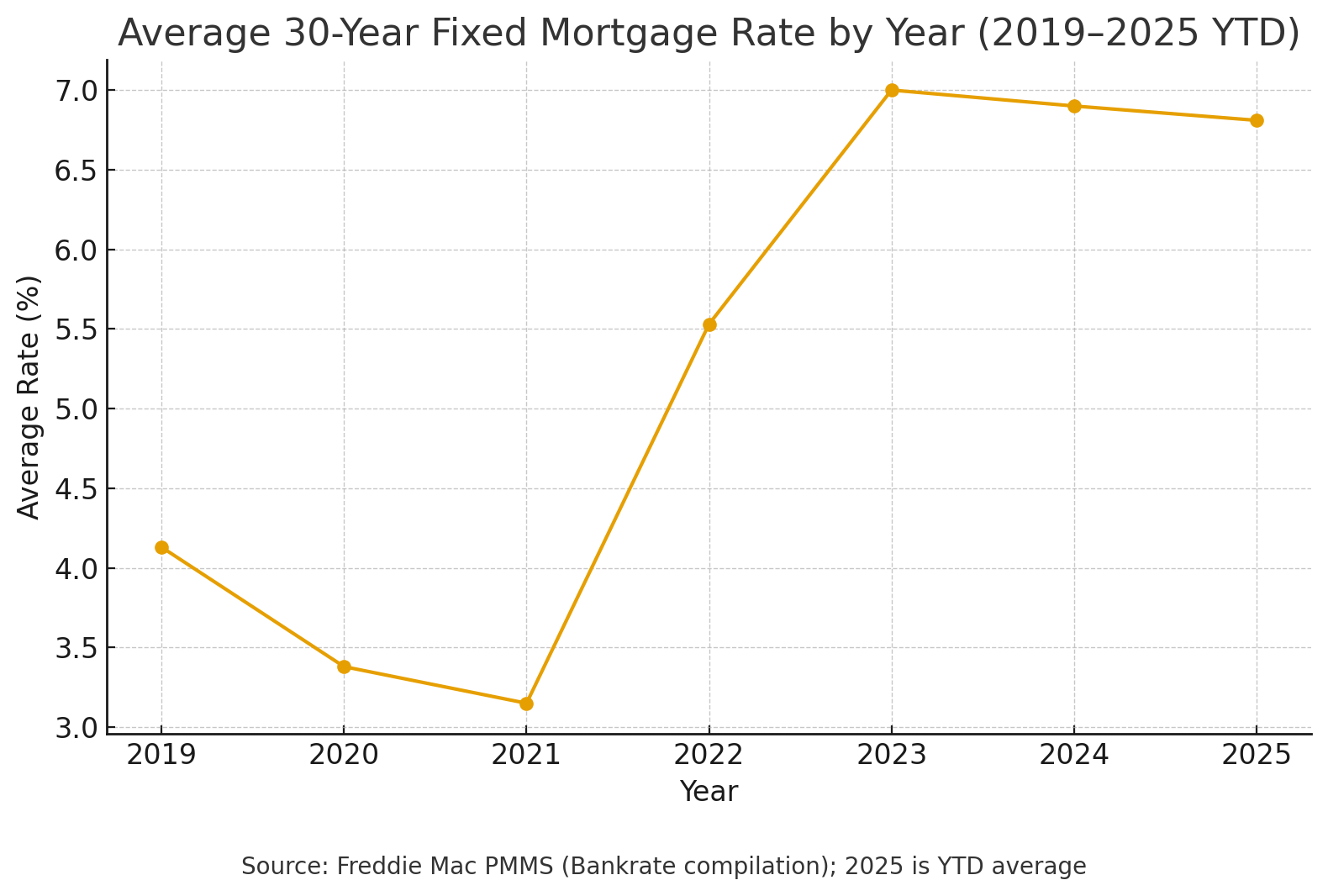

For context, here’s the annual average trend (Freddie Mac PMMS as compiled by Bankrate):

2019: 4.13%

2020: 3.38%

2021: 3.15%

2022: 5.53%

2023: 7.00%

2024: 6.90%

2025 YTD: 6.81% (Bankrate)

Why this matters: Rate direction affects affordability, cash flow, and cap rates (through the cost of debt). Although simple theory says cap rates should track interest rates one-for-one, empirical studies find the relationship is more complex, with risk premia and income growth also driving pricing. (CFA Institute Daily Browse)

Home prices and supply

NAR’s latest Existing-Home Sales snapshot shows August 2025 sales at a 4.0M SAAR with a $422,600 median price (+2.0% YoY) and 4.6 months of inventory—still a relatively tight market by historical standards. (National Association of REALTORS®)

On the repeat-sales side, the S&P CoreLogic Case-Shiller National Index (NSA) printed 331.13 in July 2025, near record levels. (FRED)

Why prices proved sticky: The oft-cited “lock-in effect”—owners sitting on ultra-low pandemic-era mortgages—has crimped resale supply, supporting prices even as mortgage rates rose; research linked to the FHFA quantifies sizable effects on sales turnover. (Financial Times)

Rentals & Multifamily: supply wave cresting, vacancies elevated but stabilizing

After a historic construction boom, multifamily completions hit ~608,000 units in 2024, the highest since the 1980s. (National Association of Home Builders) Deliveries are slowing in 2025—RealPage projects ~431,000 units for the year as the pipeline tapers. (RealPage)

The consequence of the 2024 surge was a higher rental vacancy rate, with the U.S. rental vacancy at 7.0% in Q2 2025 (up from 6.6% a year earlier), per the Census HVS. (Census.gov)

Here’s the recent vacancy trend:

Even so, demand is firming: RealPage reported record Q2 2025 absorption (over 227,000 units), signaling that as deliveries slow, vacancy should peak and begin to edge down in many metros—albeit unevenly across submarkets and asset classes. (CRE Daily)

What peer-reviewed research says about real estate as an investment

Long-run returns: In a landmark, peer-reviewed paper in the Quarterly Journal of Economics, Jordà, Knoll, Kuvshinov, Schularick, and Taylor found that across 16 advanced economies since 1870, housing’s long-run real returns are comparable to equities, with generally lower volatility at the national level. This does not eliminate cyclicality, but it supports a strategic allocation to real estate for long-horizon investors. (OUP Academic)

Inflation hedging: Recent peer-reviewed work in the Journal of Real Estate Finance and Economics (Muckenhaupt, 2025) shows that listed real estate’s inflation-hedging efficacy depends on the regime—stronger in stable periods, weak to negative in turbulent periods—a nuance consistent with earlier literature showing mixed short-run hedging but meaningful long-run protection. (SpringerLink)

Rates and prices: Academic and agency researchers find that higher mortgage rates generally weigh on house prices, but with modest short-run elasticities and substantial heterogeneity by local supply constraints and borrower payment capacity. (See FHFA research on interest-rate pass-through and the New York Fed’s work on semi-elasticities.) (FHFA.gov)

Takeaway: Peer-reviewed evidence supports real estate as a credible long-term, inflation-aware asset—but timing and regime matter, and short-term hedging is not guaranteed. (SpringerLink)

Pros & cons of buying in 2025

Tailwinds

Rates are down from recent highs. Lower debt costs can boost DSCR and project feasibility, especially for value-add and build-to-rent strategies if you lock in attractive fixed terms or a clear refi path. (Freddie Mac)

Supply in multifamily is peaking. With 2024’s record completions behind us and 2025 deliveries declining, new-lease rent growth should stabilize or reaccelerate as absorption catches up—market by market. (National Association of Home Builders)

Long-run asset case remains solid. Peer-reviewed evidence supports housing’s competitive real returns and inflation resilience over long horizons. (OUP Academic)

Headwinds

Affordability remains stretched. Even with lower rates, monthly payments are far above 2020–2021 levels; price stickiness (helped by lock-in) limits bargain hunting in many metros. (National Association of REALTORS®)

Vacancies elevated in some Class A corridors. Sun Belt and high-construction submarkets still face lease-up pressure, concessions, and uneven rent growth—good for acquisitions at a discount, but risky if underwriting assumes fast normalization. (The Wall Street Journal)

Cap rates don’t move one-for-one with rates. Expect variability: investor risk premia, NOI growth expectations, and capital availability all influence yields. Underwrite conservatively. (CFA Institute Daily Browse)

Multifamily investors: what’s especially trending in 2025

From peak supply to digestion. The 608k 2024 completions created a temporary glut in certain submarkets (particularly luxury/high-amenity product). With 2025 deliveries dropping, the focus turns to absorption pace, concessions burn-off, and rent re-acceleration. (National Association of Home Builders)

Record absorption pockets. Select metros posted all-time demand highs by mid-2025, with Dallas and other Southern markets leading—evidence that the demand side remains resilient even after heavy supply. (RealPage)

Reading the vacancy tape. National rental vacancy at 7.0% (Q2 2025) is high versus 2021–2022 but appears near plateau as deliveries roll off. Watch submarket splits: Class A urban/sunbelt can differ markedly from workforce suburban. (Census.gov)

Debt strategy matters more than ever. With rates still ~6–7% and forward cuts uncertain, use rate caps, fixed-rate debt, or assumable loans where available, and underwrite refi DSCR with cushion. (For current rate context, see PMMS.) (Freddie Mac)

Two data visuals to anchor your decision

Average 30-Year Fixed Rate (2019–2025 YTD)

This chart shows how borrowing costs reset higher after 2021 and have eased in 2025, improving acquisition math versus late 2023. (Bankrate)

2. U.S. Rental Vacancy (2020–2025 Q2)

Vacancy rose with the supply surge, but with deliveries slowing and record Q2 absorption, many markets are positioned for gradual tightening—subject to local conditions.

(Census.gov)

How to decide: a practical checklist

1) Clarify your real estate investing strategy.

Are you targeting buy-and-hold rentals, value-add multifamily, short-term rentals, or house hacking? Long-run investors benefit most from real estate’s inflation-aware cash flows and equity build-up, consistent with peer-reviewed evidence on returns. (OUP Academic)

2) Underwrite today’s debt markets, not yesterday’s.

Stress test: DSCR at +100–150 bps over your rate, rent growth at/under CPI, and cap rate expansion at exit. Remember cap rates may not track rates 1:1; include risk premia shifts in scenarios. (CFA Institute Daily Browse)

3) Buy where supply is rolling off and demand is sticky.

Look for absorption > deliveries, durable employment/in-migration, and barriers to new supply. Many 2024 over-supply metros are now normalizing, but submarket selection is crucial. (RealPage)

4) For multifamily, watch concessions and lease-trade-out.

Elevated vacancy is not a blanket red flag; it can be an entry opportunity if you underwrite a slow, realistic stabilization (and fund the carry). National vacancy at 7.0% is the starting point—dig into submarket data. (Census.gov)

5) Favor fundamentals over timing.

Peer-reviewed results show housing’s long-run return profile is competitive; attempting to perfectly time rate cycles is less important than buying well, operating well, and holding long enough. (OUP Academic)

FAQs investors are asking in 2025

Is it smarter to wait for sub-6% mortgages?

If your deal only works at sub-6% rates, the deal is too tight. Underwrite to today’s rates with buffers. If rates fall further, that’s “alpha.” If not, your plan still pencils. Current PMMS levels are ~6.3%. (Freddie Mac)

Are multifamily deals dead because vacancy is up?

Not broadly. 2024’s record completions pushed vacancies higher, but 2025 supply is waning and absorption is robust in several metros. It’s a stock-and-flow story: as supply normalizes, effective rent growth should stabilize. (National Association of Home Builders)

Does real estate still hedge inflation?

Short-term: mixed. Long-term: supportive. Peer-reviewed research shows listed real estate hedges inflation better in stable regimes, and long-run housing returns stack up well versus equities. (SpringerLink)

The verdict

Yes— for patient, fundamentals-driven investors with prudent leverage, now can be a good time to invest in real estate. Rates have eased from the 2023–2024 highs, resale inventory is tight (supporting prices), and in multifamily the once-in-a-generation supply wave appears to be peaking, setting the stage for gradual re-tightening as 2025 progresses. The peer-reviewed literature supports real estate as a long-run, inflation-aware asset, but it also warns that short-run hedging is inconsistent, and that outcomes depend on regime and market selection. Underwrite conservatively, prioritize location and durable NOI, and structure debt with downside protection. (Freddie Mac)

Sources

Freddie Mac PMMS: weekly mortgage rates & archives. (Freddie Mac)

Bankrate compilation of annual averages: 30-year fixed by year (based on Freddie Mac). (Bankrate)

NAR Existing-Home Sales: August 2025 price, inventory, and sales. (National Association of REALTORS®)

S&P CoreLogic Case-Shiller (FRED): U.S. National Index. (FRED)

Census HVS: Q2 2025 rental vacancy. (Census.gov)

NAHB/Census: Multifamily completions (2024 record). (National Association of Home Builders)

RealPage: 2025 delivery forecast & Q2 absorption surge. (RealPage)

Peer-reviewed:

Jordà et al. (2019), QJE, “The Rate of Return on Everything, 1870–2015.” (OUP Academic)

Muckenhaupt (2025), Journal of Real Estate Finance and Economics, “Listed Real Estate as an Inflation Hedge Across Regimes.” (SpringerLink)

Additional context on rates, prices & cap rates: CFA Institute piece on cap rates vs rates; NY Fed on mortgage-rate semielasticities; FHFA interest-rate pass-through. (CFA Institute Daily Browse)