What Does the 2026 Landscape Look Like for Multifamily Real Estate?

Introduction: As we enter the new year, apartment investors face a multifamily landscape at an inflection point. The past few years saw unprecedented conditions – from a construction boom and rapid rent surges to interest rate shocks and cooling demand. Now, cautious optimism is emerging in the industry, buoyed by expectations of improving fundamentals and potential relief from economic headwinds urbanland.uli.org. In this outlook, we examine the key trends shaping U.S. multifamily real estate in the year ahead. We focus on national-level insights from the cresting wave of new supply and evolving tenant demand, to interest rate impacts, rent growth projections, cap rate movements, and the readiness of institutional capital.

Supply Surge Easing After Record Completions

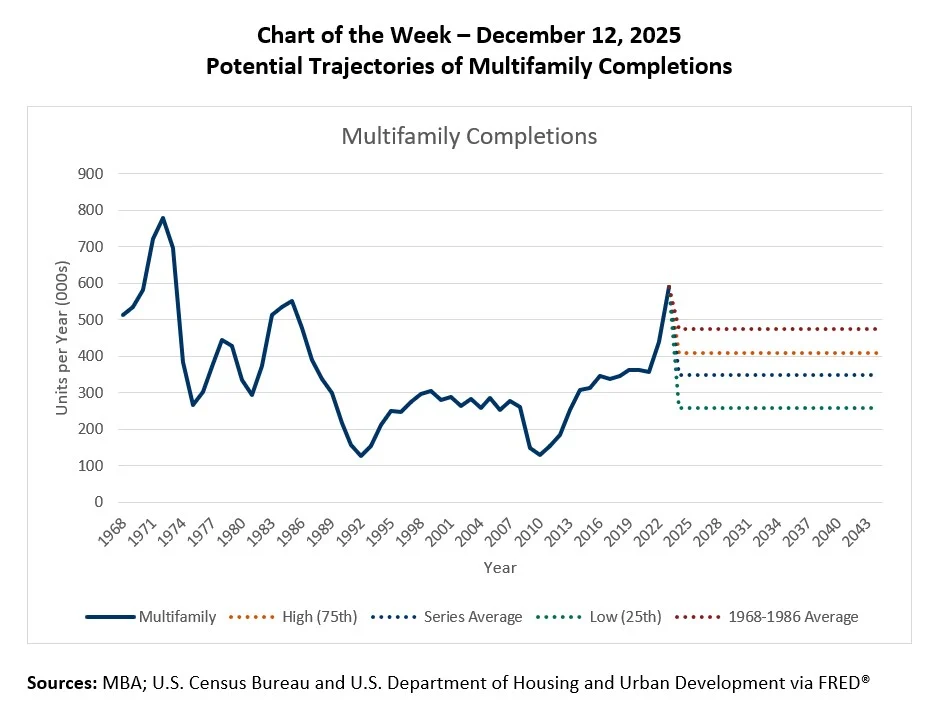

Few trends will influence 2026 as much as the supply pipeline. Developers delivered a flood of new apartments in recent years, reaching levels not seen in five decades. In fact, 2024 completions approached 600,000 units nationally. This is the second-highest volume on record after 1972 mba.org. (Industry estimates from Yardi Matrix put 2024 new supply even higher, at over 685,000 units, a 53.7% increase from 2021’s level multifamilydive.com.) This construction boom, largely a result of projects initiated during the 2021–2022 frenzy, has expanded rental inventories at a historic clip. Over the past three years, a record pace of more than 1.4 million apartments have been added nationally marcusmillichap.com. Importantly, much of this new development has been concentrated in Sun Belt and Mountain region markets, some of which grew their rental stock by nearly 20% in just three years cbre.com.

Despite the sheer volume of new deliveries, the pipeline is finally beginning to taper. Most high-supply metros have likely passed their peak delivery year (many peaked in 2023 or 2024), and nationwide apartment completions are expected to decline in 2025 and 2026 cbre.comyardi.com. Yardi Matrix forecasts roughly 585,000 units will be delivered in 2025, dropping to about 441,000 in 2026 multifamilydive.com. This still represents robust construction activity by historical standards, but a notable downshift from the recent apex. In fact, the number of units under construction has already fallen significantly. By late 2025, the active construction pipeline was about 53% smaller than at its peak in 2023 marcusmillichap.com. This is a clear sign that developers pulled back on new starts as market conditions cooled.

Figure: U.S. Multifamily Completions per Year – 1968 through 2024, with Projected Ranges Beyond. (Source: Mortgage Bankers Association analysis) mba.org.

For investors, this easing supply picture carries a dual message. In the short term, elevated deliveries are creating pockets of oversupply that temper rent growth and lift vacancies in certain markets. Nowhere is this more evident than in some Sun Belt cities, where a glut of new units has temporarily pushed vacancy rates almost 200 basis points higher than in regions with less construction marcusmillichap.com. Heavily developed metros like Austin, Houston, Charlotte, Phoenix, and others that boomed during 2021–2022 have even seen average effective rents inch down over the past three years amidst fierce competition from new buildings marcusmillichap.com. However, the longer-term outlook is constructive. The fact that development starts are decelerating sharply (mid-2025 multifamily starts were ~74% below their 2021 peak) cbre.com means that after the current wave of lease-ups, supply growth will moderate. Many high-supply markets are already seeing light at the end of the tunnel: as completions slow, occupancy has begun to recover, and markets that saw negative rent growth in 2023–2024 are expected to turn positive as we head into 2025 cbre.com. In summary, 2024 marks the tail end of a record construction surge. Investors should anticipate continued near-term inventory expansion – which may pressure rents in overbuilt locales – but also welcome the brewing lack of new supply by 2025–2026 that could tighten market conditions thereafter.

Demand and Occupancy: Resilient Fundamentals Amid Headwinds

On the demand side, apartment fundamentals are navigating a more complex picture. The good news is that tenant demand has remained positive. Overall, there is little evidence of the kind of collapse in absorption that some feared when supply spiked. In fact, the recent supply wave was met by an unprecedented level of rental housing demand, which helped keep vacancy rates in check marcusmillichap.com. Nationwide vacancy did rise off historic lows, but only to the mid-4% range before leveling off. Marcus & Millichap notes the U.S. vacancy rate peaked in early 2024 and then edged down to 4.6% by Q3 2025, a sizable improvement of 130 basis points from that peak marcusmillichap.com. Similarly, CBRE reported vacancy of 4.4% in Q3 2025 after new deliveries briefly outpaced absorption cbre.com. This is a sign that demand has broadly kept pace even as supply hit its apex. In other words, renters have absorbed a large share of the new units coming online, preventing a supply-driven glut at the national level.

That said, demand did soften in 2023–2024 compared to the red-hot period immediately after the pandemic. A combination of economic and demographic factors pumped the brakes on renter household formation. Job growth decelerated in mid-2025, and consumer confidence wavered amid talk of recession. These are conditions that likely caused some young adults to delay moving out or doubling-up rather than signing new leases yardi.comcbre.com. The key 20–28 year-old renter cohort saw its unemployment rate jump to 7.4% in 2025 (vs ~4.4% overall) as certain industries slowed hiring marcusmillichap.com. At the same time, the pandemic-era trend of people relocating to Sun Belt cities lost some steam: domestic migration to many Southern metros has tapered from the peak levels seen a few years ago marcusmillichap.com. These dynamics translated into weaker apartment absorption in 2024–2025 than in previous years. For example, Q3 2025 net absorption was down ~73% year-over-year, the lowest Q3 demand since 2022 cbre.com. In pockets of oversupply, a short-term supply-demand imbalance emerged, with new buildings leasing up more slowly than anticipated yardi.com. All of this pushed vacancies higher in Sun Belt markets and forced landlords in those areas to offer rent discounts to attract tenants.

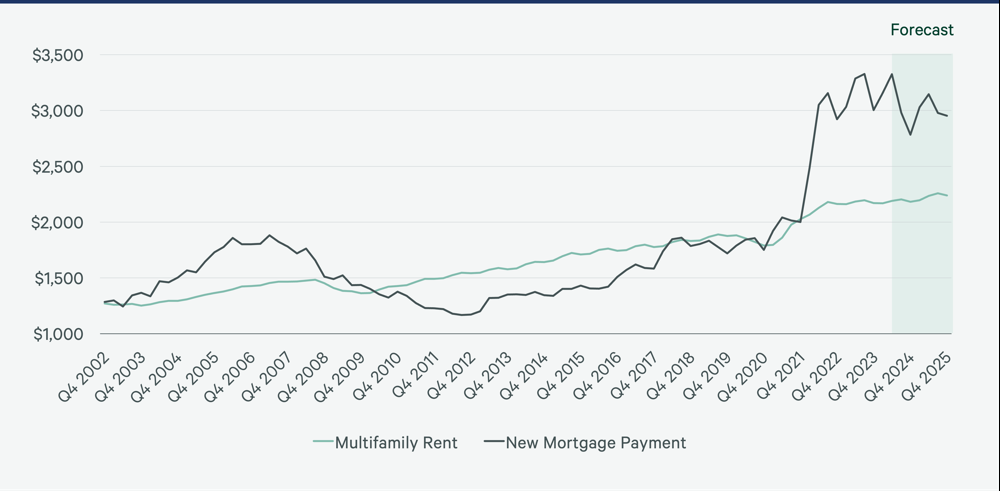

Crucially, long-term demand drivers for multifamily remain firmly intact, and in some ways have strengthened. One major factor is the ongoing affordability crisis in the for-sale housing market. High mortgage rates and elevated home prices have made homeownership prohibitively expensive for many renter households. As of late 2024, the monthly payment on a median-priced home was roughly $1,200 more than the average apartment rent marcusmillichap.com. In large coastal markets, buying can cost two to three times what renting does on a monthly basis cbre.com. This wide cost-to-buy premium will continue to favor renting: many would-be first-time homebuyers are staying in the renter pool longer because they simply cannot afford to purchase a house cbre.com. In fact, industry forecasts expect the rent-versus-buy gap to remain historically large even as interest rates gradually ease, keeping today’s renters in rentals for longer cbre.com. The effect is already visible: lease renewal rates have been running around 55% (above the long-term average) as more renters choose to stick with their apartments rather than brave the costly buyers’ market marcusmillichap.com.

Figure: Average U.S. Monthly Apartment Rent vs. Monthly Home Mortgage Payment. (Source: CBRE Econometric Advisors, Q3 2024) cbre.comcbre.com.

Demographics also underpin steady apartment demand. The U.S. is still adding new households (albeit more slowly), and immigration, while reduced in recent years, is projected to contribute to population growth that supports housing formation urbanland.uli.org. Even where young adults have delayed setting out on their own due to economic uncertainty, that demand is viewed as deferred, not lost; as the job market stabilizes, many of those doubled-up or sidelined renters will move into apartments marcusmillichap.com. In short, there remains a structural need for housing, especially in affordable price tiers and growing metro areas. Indeed, industry research points out that despite short-term headwinds, the multifamily sector benefits from significant tailwinds: high costs of homeownership, an ongoing housing undersupply in many cities, and the flexibility/renter-by-choice preferences of a portion of the population marcusmillichap.com cbre.com.

Regional demand trends bear mentioning. During 2024, lower-cost secondary and tertiary markets with limited new construction generally outperformed the big, high-growth markets that were flooded with supply mf.freddiemac.com cbre.com. For instance, the Midwest and many Northeast metros did not see their vacancy rates breach historical averages by nearly the degree Sun Belt markets did cbre.com. These are supply-constrained, often more affordable markets maintained healthier occupancies and even logged solid rent gains. Entering 2024, many Midwest/Northeast cities are expected to achieve annual rent growth above 3%, outperforming the nation cbre.com. In contrast, Sun Belt hubs (and a few Mountain West cities) are still digesting new inventory and may lag slightly until their demand catches up in late 2024 or 2025 cbre.com. Nonetheless, even in the most oversupplied locales, there are signs of a turnaround: landlords report that demand has picked up as they offer competitive concessions, and the out-migration from expensive coastal cities has slowed or reversed (e.g. New York’s population decline post-2020 has stabilized) urbanland.uli.org urbanland.uli.org. The bottom line is that national multifamily demand remains fundamentally sound. Short-term economic jitters and regional supply gluts are tempering absorption right now, but rental housing continues to benefit from an economy near full employment and the enduring relative need for rental units given the alternatives. Investors should monitor local job and migration trends, yet remain cognizant that the broader renter pool is still growing, and poised to reaccelerate if and when consumer confidence improves marcusmillichap.com.

Interest Rates and Financing: Highs Plateauing, Eyes on the Fed

Perhaps no factor loomed larger over multifamily investing in the past two years than interest rates. Rapid Federal Reserve rate hikes from 2022 into 2023 sharply raised borrowing costs, squeezed deal underwriting, and cooled investment activity across commercial real estate. By late 2023, however, the interest rate environment had entered a new phase: a plateau, followed by hints of relief. The Fed’s benchmark rate peaked in 2024 and has since been held steady, with industry expectations that further rate cuts could materialize heading into 2025 and 2026 urbanland.uli.org. Indeed, the Urban Land Institute’s Emerging Trends survey notes “additional interest rate cuts” are anticipated by many market participants, contributing to a cautiously optimistic industry outlook urbanland.uli.org urbanland.uli.org. While nothing is guaranteed, the prevailing baseline among economists is that inflation will continue moderating toward ~3% or lower, allowing the Fed to gradually ease policy rates over the next 12–24 months fanniemae.com fanniemae.com.

Concretely, mortgage rate forecasts for the end of 2025–2026 are in the high-5% range, down from the 6.5–7% levels seen at the peak of 2023 fanniemae.com fanniemae.com. Fannie Mae, for example, projects the 30-year fixed mortgage rate to tick down to around 5.9% by Q4 2026 (from roughly 6.3% at end of 2025) fanniemae.com. While multifamily lending rates differ from single-family, they move directionally with the broader rate environment. Any moderation in the 10-year Treasury yield and credit spreads will translate to lower all-in loan rates for apartment acquisitions and refinancing. Yardi Matrix analysts likewise expect a “moderate reduction in short-term interest rates” in 2026 and beyond multifamilydive.com, which would provide some breathing room for developers and owners facing higher debt costs. This suggests that 2024 could usher in the beginning of an easing cycle, however incremental, after the most rapid rate tightening in decades.

Even if interest rates stay elevated relative to the 2010s, rate stability itself is a welcome development for investors. The volatility and uncertainty of 2022–2023 kept many buyers and lenders on the sidelines. Now, with the Fed pausing hikes and inflation trending down, debt markets have a clearer outlook for underwriting. Freddie Mac noted that a stable interest rate environment – even at higher levels – can help spur transaction volume because it reduces the risk of sudden financing changes mf.freddiemac.com. We are already seeing evidence of this: as 2024 began, the pace of multifamily dealmaking picked up from the prior year’s lull, coinciding with more predictable financing costs. Moreover, lenders are increasingly eager to put out capital again – both traditional banks (notwithstanding some recent turmoil in regional banks) and the GSEs. For 2024, the Federal Housing Finance Agency actually raised the lending caps for Fannie Mae and Freddie Mac to $75 billion each (and to $88 billion each for 2025), reflecting confidence in the multifamily sector and a need to support loan refinances cbre.com mf.freddiemac.com. Agency lenders continue to offer attractive terms, especially for mission-driven and affordable housing loans, ensuring that credit is available for viable projects.

Of course, investors must still navigate the reality of higher financing costs than those prevalent a few years ago. All-in interest rates for permanent multifamily loans that were ~3–4% in 2021 became 5–6% (or higher) in 2023–2024, dramatically changing underwriting math. This has pressured property values and required larger equity checks for acquisitions. Many owners with floating-rate debt saw debt service spike, and an upcoming wave of loan maturities will require refinancing at these higher rates. Some distress has begun to emerge for over-leveraged assets (especially newer developments that leased up slower than expected). However, regulators and lenders have shown flexibility. For example, banking regulators have encouraged loan modifications to prevent unnecessary foreclosures on fundamentally sound assets. If interest rates indeed plateau and gradually decline in 2024–2025, it will alleviate a major headwind: refinancing activity should increase, and fewer properties will be caught in untenable debt situations.

In summary, 2024’s interest rate outlook is cautiously positive for apartment investors. We are transitioning from an era of rate shocks to one of relative stability, with the possibility of mild relief. This should bolster investor confidence and liquidity in the market. Capital markets are already thawing, but by late 2025, multifamily investment lending was rising again cbre.com. Still, prudence is warranted. The Fed remains data-dependent, and any resurgence of inflation or economic overheating could delay rate cuts. Conversely, a sharper-than-expected economic slowdown might prompt faster easing but also dent housing demand. Thus, investors should stay alert to macroeconomic signals. Overall, though, the expectation is that financing conditions in 2024 will be more favorable than the prior year, turning what was a severe obstacle into more of a neutral factor – and potentially a tailwind by 2025 if borrowing costs inch down further.

Rent Growth: Modest Gains Now, With Potential to Accelerate

After the roller-coaster of rent growth in the early 2020s, the apartment market is entering a period of measured, modest rent gains; at least in the near term. During the pandemic rebound, annual rent growth hit extraordinary highs (over 10% nationally in 2021 and into 2022 in many markets). That pace proved unsustainable. By 2023, rent growth had downshifted to low single-digit territory, and 2024 continued the trend of normalization. For example, as of Q3 2025, year-over-year effective rent growth was running at just +0.5% nationally (essentially flat from the prior quarter) cbre.com. U.S. asking rents even declined slightly in late 2025 on a monthly basis. November 2025 saw the fourth consecutive month of slight rent drops, leaving the national average rent only 0.2% higher than a year prior yardi.com. Industry analysts attribute this stagnation to the supply-demand imbalance in many cities (a surge of new deliveries facing tepid demand under weak consumer confidence) combined with normal seasonal weakness in winter months yardi.com. In plain terms, rent growth hit a soft patch in 2024–2025 as the market absorbed a wave of new units.

Looking ahead, expect 2024 rent growth to remain positive but modest on a national level. Most forecasts cluster in the low-single-digit range for the coming year. Yardi Matrix, for instance, projects only about a +1.2% increase in U.S. average rents for 2026 yardi.com (and by extension a similar modest pace in 2024–25). This baseline assumes that while supply headwinds and economic uncertainty persist, they are enough to keep rents growing slower than inflation. Similarly, Freddie Mac’s outlook anticipated below-average rent growth in 2024 given the high rate of new supply coming online mf.freddiemac.com mf.freddiemac.com. Many investors are underwriting roughly 2% to 3% annual rent growth in the next few years on acquisitions cbre.com, which is a comedown from the 5%+ they might have assumed back in 2021. In essence, the industry is bracing for “low growth but stability”, an environment where rents inch up at a restrained pace, reflecting competitive leasing conditions in many markets.

There is, however, a case to be made that rent growth could accelerate later in 2025 and especially into 2026. The optimistic scenario hinges on the supply tapering discussed earlier and the expectation of continued strong housing demand. CBRE’s analysis argues that as the construction pipeline shrinks and the economy steadies, “strong renter demand will lower the vacancy rate and precipitate above-average rent growth in 2026.” cbre.com cbre.com Markets that were under pressure from record deliveries should see fundamentals improve once those deliveries subside. In fact, many high-supply markets are expected to see rent growth turn positive again in 2024–2025 after experiencing a dip cbre.com. By 2026, CBRE forecasts U.S. rent growth could rise above the pre-pandemic norm of ~2.7% annually, potentially averaging around 3% or slightly higher for a few years cbre.com. This is predicated on job growth and household formation reviving (no recession), and on landlords regaining pricing power as vacancies tighten back up. It’s worth noting that in markets with less new construction, especially parts of the Northeast, Midwest, and select coastal cities, rent growth is already expected to exceed 3% in the near term cbre.com. Those markets offer a preview of what could happen nationally: with fewer new units to compete with, landlords can more confidently raise rents in line with incomes.

Another factor that could influence rent trajectories is affordability and consumer capacity. Even though renting is cheaper than buying, renters are facing affordability challenges of their own. Rent-to-income ratios have climbed in recent years, and inflation in non-housing costs (like food and energy) squeezes renter budgets. There is a practical ceiling to rent growth in many metros, especially Class B/C segments where tenants can only bear so much. This is why rent increases are expected to remain relatively moderate, and landlords simply can’t push rents aggressively without causing higher turnover or delinquencies. The silver lining is that any softening in rent growth helps improve affordability a bit, which can sustain occupancy. Additionally, if wage growth outpaces rent growth (as it has in 2023/24 in some regions), renters’ ability to absorb modest rent hikes improves, possibly giving room for slightly faster rent growth down the line.

In balancing these considerations, the consensus seems to be: plan for another year of mild rent growth overall, but be prepared for a potential uptick beyond that. In numbers, that could mean national rents rising on the order of 2% in 2024 (plus or minus), and perhaps 3%–4% in 2025 if conditions strengthen. Notably, “all markets are expected to see rising occupancies and accelerating rent growth by 2025” according to CBRE’s 2025 outlook cbre.com, even if the magnitude varies. Thus, 2024 could be something of a turning point – the year where rent growth bottoms out and then transitions back toward a more normal (or even above-normal) range as the excess supply is worked through. For apartment investors, this means underwriting should remain conservative in the short run, but there is cause for measured optimism that rent growth will regain momentum in the medium term. Properties in markets with constrained supply or in-demand affordable price points may outperform the averages. Conversely, assets in overbuilt submarkets might need another few quarters (and perhaps incentives) to achieve rent increases. Overall, the era of double-digit rent spikes is behind us, but so too, it seems, is the brief era of flat rents. The baseline is a return to positive, sustainable growth.

Cap Rates and Valuations: Finding a Floor and Potentially Firming Up

Apartment cap rates, a critical valuation metric, have undergone a noticeable recalibration alongside interest rates. During the ultra-low rate environment up through 2021, multifamily cap rates compressed to record lows (many prime assets traded at sub-4% cap rates). The surge in interest rates since 2022 reversed that trend, driving cap rates higher (and values lower) as investors demanded higher yields. The question now is how cap rates will behave in 2024, given that interest rates may have peaked and investor sentiment is improving. The evidence suggests that cap rates are stabilizing and could even compress slightly in the coming year, barring any adverse economic shifts.

Data from 2025 indicates that cap rates likely peaked around late 2023 or early 2024 for multifamily. By mid-2025, as the market found its footing, cap rates had actually ticked down a bit. According to CBRE’s survey of major markets, the average going-in cap rate for core multifamily assets fell to 4.75% in Q2 2025, a 6 basis point compression from the previous quarter cbre.com. The average exit cap rate (i.e. reversion at sale) likewise dipped to ~4.96%. This slight cap rate compression occurred even as the Fed held interest rates steady, reflecting improved investor confidence and a competitive bidding environment for high-quality properties cbre.com cbre.com. In other words, cap rates did not continue climbing in 2025 despite still-elevated interest rates. This is a sign that the market had already priced in the rate environment and was looking ahead to a more stable future. Industry sentiment surveys reinforce this: by early 2025, 65%+ of multifamily investors expressed neutral-to-positive sentiment on valuations, and far more buyers saw opportunity after the price corrections of 2022–23 cbre.com. This translated into a perception that “cap rates may have peaked”, with many investors now expecting relative stability in cap rates going forward credaily.com.

For 2024, the outlook is that cap rates will flatten out and potentially begin compressing (reducing) if interest rates indeed retreat. The cap rate is fundamentally linked to the risk-free rate (Treasury yields) and financing costs; if those decline, property yields become more attractive and competitive pressures can drive cap rates down. CBRE anticipates that as the Fed starts cutting rates over the next two years, going-in cap rates will compress more than exit cap rates, widening the spread between entry and exit yields cbre.com cbre.com. This scenario implies that buyers in 2024–25 might acquire at slightly higher yields, but expect to exit at only modestly higher cap rates once the market fully recovers. In practical terms, many investors are underwriting flat or only +25 bps higher exit cap rates five years out cbre.com, demonstrating a belief that today’s cap levels already contain a cushion and big further jumps are unlikely. For core assets in top markets, a mid-4% cap might represent the new normal pricing, absent a major change in interest rates or rent growth prospects.

It’s also instructive to consider cap rate spreads, the premium of cap rates over benchmarks. In late 2023, cap rate spreads had tightened uncomfortably as Treasury yields rose faster than cap rates (many deals saw spreads well under 200 bps). Freddie Mac warned that these tight spreads could put upward pressure on cap rates if sustained mf.freddiemac.com. Fortunately, as of 2024 we’ve seen some relief: either Treasury yields have come off highs or cap rates have adjusted enough to restore a more typical spread. With a 10-year Treasury in the ~4% range and multifamily caps around 5% (roughly speaking), the spread is closer to historical norms now. If the 10-year yield falls to, say, 3.5% and cap rates hold around 4.75–5.0%, spreads would widen again, potentially prompting cap rate compression as competition intensifies. Indeed, cap rate surveys show slight declines in H1 2025 across many markets yieldpro.com. All of this points to an environment where valuations are finding a floor. The dramatic price discovery of the past two years, which saw apartment values drop perhaps 15–25% from their 2021 peaks in many cases, has brought out buyers who feel pricing is now fair relative to income and replacement cost.

For investors, this means 2024 could be an opportune time to lock in acquisitions before cap rates possibly compress again. Even a 25–50 bps compression can significantly boost value on exit. However, one should remain vigilant: if the economy falters or debt costs unexpectedly rise, cap rates could move up again. Cap rates for value-add and secondary market assets are a bit higher (often in the 5–6% range) and might be slightly more volatile if risk appetite shifts cbre.com. But generally, expect cap rates to be more stable in 2024, ending the wild swings of the prior period. The multifamily sector’s inherent stability, strong occupancy, steady cash flows, means it tends to attract capital quickly when prospects brighten, which in turn supports valuations. In fact, as noted earlier, multifamily is the top preferred asset class for investors currently cbre.com, suggesting there will be ample bidders keeping cap rates in check. In summary, cap rates are likely at or near their cyclical high, and the path of least resistance in 2024–2025 is sideways or downward (i.e. valuation upside). Apartment investors should thus feel more confident in pricing, with less fear that values will erode further; a crucial consideration for both buying decisions and refinancing plans.

Institutional Investment: Dry Powder on the Sidelines Poised to Re-Engage

One of the most encouraging signals for apartment investors going into the new year is the stance of institutional capital. Throughout the recent volatility, large investors (from private equity real estate funds to insurance companies, pension funds, and REITs) have maintained a strong underlying interest in the multifamily sector. Now, with the market outlook improving, those institutions are gearing up to deploy capital at scale. Simply put, multifamily remains the darling of commercial real estate investment allocations, and 2025/2026 may see a resurgence of big-money activity in the apartment arena.

Surveys consistently show that investors rank multifamily as a top (if not the top) target. CBRE’s 2025 outlook explicitly stated: “with continued solid fundamentals, multifamily is the most preferred asset class for commercial real estate investors in 2025.”cbre.com This sentiment stems from apartments’ proven resiliency (evidenced by low default rates and relatively quick recoveries after disruptions) and from secular tailwinds like the U.S. housing shortage and favorable renter demographics. Even during the capital markets slowdown of 2022–2023, institutions were waiting in the wings. Many adopted a “wait until pricing adjusts, then buy” strategy. As a result, a significant amount of “dry powder” capital has been raised for real estate, much of it earmarked for multifamily acquisitions once attractive opportunities arise.

We are now starting to see the fruits of that capital readiness. Investment sales volume in the multifamily sector has begun to rebound. Through the first three quarters of 2025, U.S. apartment investment reached $108 billion, up 7.5% year-over-year cbre.com. If one excludes a huge portfolio acquisition in 2024 (Blackstone’s purchase of a major REIT), 2025’s deal volume was actually nearly 20% higher than the same period the year prior cbre.com. This is a striking turnaround, suggesting that investors are coming off the sidelines. A key driver is that the bid-ask spread is narrowing. Sellers have adjusted pricing to the new reality, and buyers, armed with abundant capital, are stepping in to meet that pricing (especially for high-quality assets or those with value-add upside). Institutional investors are also motivated by a strategic imperative: many view the current moment as an opportunity to buy into multifamily at a relative discount (compared to the frothy values of 2021) before growth reaccelerates. As one industry CEO observed, the “appetite for buying is at a 20-year high” heading into 2026 urbanland.uli.org. That is a remarkable statement, underscoring how much capital is eager to increase exposure to apartments if the conditions are right.

Lending trends reinforce this narrative. Not only is equity interested, but debt capital is widely available for multifamily as well. Banks and alternative lenders are selectively financing deals, and the agency lenders (Fannie Mae and Freddie Mac) have plenty of capacity to purchase loans. In fact, Freddie Mac’s multifamily loan purchase cap for 2026 is set at $88 billion (similar for Fannie Mae), signaling that the GSEs expect robust lending volume and are committed to supporting the sector mf.freddiemac.com. Meanwhile, debt funds and life insurers have also indicated a willingness to finance solid multifamily projects, often quoting loans for stabilized assets in the low-to-mid 5% interest rate range (subject to change with Treasury moves). Liquidity is returning to the apartment investment market, thanks to this combination of eager equity and accommodative lenders. Yardi’s latest outlook noted that “multifamily has abundant capital for acquisitions” and that the deal momentum seen in late 2025 is likely to continue into the new year yardi.com yardi.com. It went so far as to say lenders are as eager as equity investors to put out capital – a far cry from the caution of a year prior yardi.com.

What does all this mean for investors on the ground? For one, competition for quality apartment assets may intensify in 2026. Core institutional players who sat out the uncertainty are now bidding again, particularly on large portfolios or assets in key growth markets. This could lead to bidding wars and firmer pricing for top-tier properties (consistent with the stabilization of cap rates we discussed). Secondly, the influx of capital could drive more creative deal structures. We might see an increase in joint ventures, preferred equity investments, or recapitalizations of existing projects as those with cash partner with those with assets. Additionally, some distressed or underperforming properties could be acquired by opportunistic funds that have been waiting for distress opportunities; these groups are well-funded and ready to move quickly on discounted sales or loan sales.

Finally, the robust institutional interest bodes well for the long-term health of the multifamily sector. It signals confidence in the asset class’s fundamentals. Institutions typically invest with a 5- to 10-year horizon (or longer for some core holders). The fact that they are bullish on apartments indicates expectations of solid rent growth, stable occupancy, and liquidity over that horizon. As investors, aligning with this “smart money” sentiment can be reassuring. Of course, it’s important to execute due diligence. Not every deal will be a winner simply because capital is available. But in aggregate, the wave of institutional capital poised to flow into multifamily in 2024 is a positive signal. It means there will be exits for those looking to sell (at respectable pricing), financing for those looking to buy or refinance, and overall, a level of demand for apartment assets that should underpin values. In short, the new year signals a renewed vote of confidence from the biggest players in real estate: they see opportunity in multifamily, and they’re gearing up to act on it.

Conclusion: Key Takeaways for Apartment Investors in the New Year

2024 is shaping up to have been a transition year for the U.S. multifamily market. Transitioning from a phase of rapid expansion and correction into a phase of equilibrium and gradual growth. For apartment investors, the overarching outlook is one of guarded optimism. On the one hand, certain challenges that marked the recent past will persist in the short term: new supply will continue to come online at elevated levels for a few more quarters, and rent growth will likely remain subdued in many markets until that supply is absorbed. The economic backdrop, too, while improved, is not without risk. Interest rates are high (if stabilizing) and the trajectory of the broader economy could influence renter demand. These factors call for discipline and careful market selection in any investment decisions.

On the other hand, the worst of those headwinds appear to be behind us. Key fundamentals are moving in a favorable direction. Supply: The development wave that caused heartburn is finally cresting, and a steep drop in new starts means relief is in sight, especially by 2025–2026 multifamilydive.com marcusmillichap.com. Demand: Despite a soft patch, underlying rental demand is intact and poised to strengthen with any uptick in the economy. Millions of millennials and Gen Z young adults still need housing, and the cost of buying a home remains a prohibitive hurdle for many, keeping them in the renter pool marcusmillichap.com cbre.com. Interest rates: The financing environment is stabilizing, with the potential for lower borrowing costs on the horizon, which should improve deal viability and reduce refinancing stress multifamilydive.com fanniemae.com. Rent growth: While modest in the immediate term, rents are still rising, not falling, nationally, and as the market rebalances, there is credible upside for rent growth to return to ~3% or better in coming yearscbre.comcbre.com. Cap rates: Valuations have adjusted and seem to have found a floor. Investors no longer expect significant cap rate expansion, and many anticipate cap rate compression if conditions hold steady cbre.com cbre.com. And importantly, investor sentiment and capital availability have improved markedly. Multifamily is attracting capital and is set to benefit from both institutional investors and lenders who are eager to increase their exposure in 2026 cbre.com yardi.com.

In summary, the new year signals a period where apartment investors can shift from defense to selective offense. Prudent strategies might include: targeting markets or submarkets where supply is limited and demand drivers are strong (for instance, workforce housing in job-growth metros or markets where new construction has pulled back); locking in financing while rates are range-bound (and potentially refinancing later if rates drop); focusing on operational excellence to capture the moderate rent increases that are available (through value-add renovations or tech and management improvements to justify rent bumps); and being ready to seize opportunities whether that’s acquiring assets at a good basis in markets that are temporarily oversupplied or partnering with groups that need recapitalization. The environment will reward investors who combine careful analysis with a long-term perspective.

The multifamily sector has weathered a challenging couple of years, but its inherent resilience is evident. Nationally, apartment occupancy is healthy, rents are inching upward, and housing shortages mean there is a built-in demand floor. As 2026 unfolds, investors should watch the trends discussed: supply deliveries and leasing velocity, Fed policy signals, capital market liquidity, and regional performance variations. as these will provide early indications of whether the market is tilting more bullish. By most indications, the apartment market is on a path of gradual improvement, not without bumps, but certainly far from the extremes of the recent past. For those with a professional, data-driven approach, 2026 offers a landscape where opportunities outweigh risks. In a phrase: cautious optimism; that is what the new year signals for apartment investors. By staying informed and agile, investors can position themselves to benefit from the multifamily sector’s next chapter of growth and stability.

Sources:

Marcus & Millichap Research Brief – 2026 Multifamily Outlook (Dec 2025) marcusmillichap.com marcusmillichap.com marcusmillichap.com marcusmillichap.com

Yardi Matrix – National Multifamily Report, November 2025 (Dec 2025) yardi.com yardi.com

Yardi Matrix – U.S. Multifamily Outlook Winter 2026 (Dec 2025) yardi.com yardi.com

CBRE – US Real Estate Market Outlook 2025: Multifamily (Nov 2024) cbre.com cbre.com cbre.com cbre.com

CBRE – Q3 2025 U.S. Multifamily Figures (Oct 2025) cbre.com cbre.com

CBRE – Multifamily Underwriting Metrics Improve in Q2 2025 (July 2025) cbre.com cbre.com

Freddie Mac – 2024 Multifamily Outlook (Nov 2023) mf.freddiemac.com mf.freddiemac.com

Urban Land Institute/PwC – Emerging Trends in Real Estate 2026 (Nov 2025) urbanland.uli.org urbanland.uli.org

Mortgage Bankers Association – Chart of the Week: Multifamily Completions (Dec 2025) mba.org

Fannie Mae Economic & Housing Outlook – (Oct 2025) fanniemae.com fanniemae.com